With enhanced Affordable Care Act subsidies set to expire at the end of 2025 after a shutdown-era stalemate, many Americans could wake up in 2026 to higher premiums—and the same old question: why does care cost so much even when you’re insured?

From TheMinuteman.org - In the last few weeks, the “health care costs” debate stopped being abstract again. People shopping for coverage through the Affordable Care Act (ACA) have been staring at a cliff: the enhanced federal help that lowers many marketplace premiums is set to expire at the end of 2025, and families are already bracing for premium shocks in 2026.

That looming deadline also collided with Washington’s most familiar ritual—funding fights that spill into shutdown threats. A recent shutdown lasted 43 days, and one of the flashpoints was what to do about the ACA subsidy extension.

So if you’re wondering, “Why is it this hard to keep coverage affordable—and what would actually fix costs long-term?” here’s the story, in plain English.

First: what’s actually happening with ACA subsidies?

The ACA created marketplaces (sometimes called “exchanges”) where individuals and families can buy private health insurance. Many shoppers qualify for premium tax credits—federal help that lowers the monthly premium.

During the COVID-19 pandemic, Congress made those tax credits more generous and expanded who qualifies. Those enhanced credits are set to expire at the end of 2025 unless Congress extends them again. Researchers and insurers warn that ending them could raise premiums sharply and push people out of coverage.

You can see the human version of that policy sentence in recent reporting: people describing plans “practically doubling,” postponing home-buying or starting a family, and even considering going uninsured because the math stops working.

States are scrambling, too. Colorado, for example, held a special session and passed a measure aimed at softening the blow—essentially emergency state-level help because federal help may disappear. But even supporters describe these as temporary patches, not a substitute for the federal scale.

That’s the setup. Now the bigger question:

Why U.S. health care costs so much in the first place

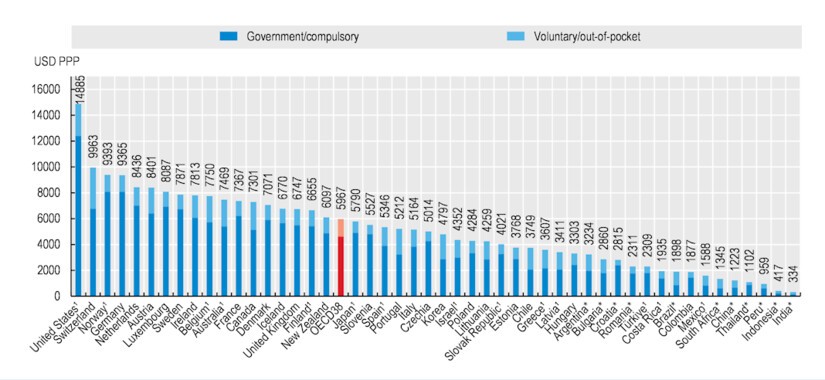

The United States isn’t just “a little” expensive—it’s in a different league.

In 2023, U.S. national health spending reached $4.9 trillion, about $14,570 per person, and 17.6% of the economy (GDP).

In 2024, the United States remained the highest spender among OECD countries at over $14,880 per person, about 2.5× the OECD average.

OECD (Organisation for Economic Co-operation and Development) is a forum and knowledge hub cooperating with over 100 countries across the globe.

Health expenditure per capita, 2024 [OECD Health Statistics 2025; WHO Global Health Expenditure Database]

The simplest explanation: we pay higher prices for the same kinds of things—hospital care, procedures, physician services, and many drugs—and we run a system with a lot of expensive complexity.

Here are the big “cost engines:”

1) Prices are high—and “market power” makes them higher

When hospitals buy up competitors or physician practices, they can negotiate higher prices with insurers. Harvard health economist Meredith Rosenthal points to consolidation (bigger systems with more leverage) as a major threat to affordability.

2) We pay a lot to move money around

America’s patchwork of insurers, billing rules, and paperwork adds a layer of administrative spending that doesn’t treat anyone. A 2023 review describes U.S. administrative health care spending as roughly $1 trillion annually.

(That doesn’t mean it’s “easy” to cut—but it tells you where the bulk is.)

3) Drugs are expensive—and competition sometimes gets delayed

One example policymakers target is “pay-for-delay”: deals where brand-name drug companies pay generic manufacturers to delay launching a cheaper alternative. The Federal Trade Commission (FTC) has long argued these deals can block competition and keep prices high.

4) Insurance design can shift costs onto patients

High deductibles and complicated cost-sharing can make people “insured” but still unable to afford health care—leading to delayed treatment, medical debt, and worse health later (which becomes higher cost later). Harvard researchers describe this affordability squeeze as a public health problem, not just a budget problem.

5) Some parts of the system are paid in ways that reward volume

In traditional fee-for-service payment (meaning health care providers get paid for each service), the system can unintentionally reward doing more—even when “more” isn’t better.

Rally in Support of the Affordable Care Act, at The White House, Washington, DC USA

Key terms (to know going forward)

Affordable Care Act (ACA): The 2010 law that expanded health care coverage through marketplaces, Medicaid expansion (in participating states), and rules for private insurance.

Premium tax credits (ACA subsidies): Federal help that lowers the monthly cost of marketplace plans for eligible people.

Out-of-network: A doctor or facility that does not have a negotiated contract with your insurer—often leading to much higher bills.

No Surprises Act: A federal law (effective January 1, 2022) that can protect consumers from certain “surprise” out-of-network bills—especially in emergencies or when you didn’t have a real choice of provider.

So…how do we fix health care costs?

There isn’t a single magic lever. But there is a realistic package of reforms that, together, can bend health care costs down while protecting coverage.

Think of it as four lanes on the same highway:

Lane 1: Protect people from cost shocks (the “can’t-wait” fixes)

These don’t solve every root cause—but they prevent immediate harm.

Extend and stabilize ACA premium tax credits so families aren’t whipsawed year to year. Experts warn that letting them expire at the end of 2025 risks health care coverage losses and major premium increases.

Cap out-of-pocket exposure more aggressively for people with serious illness (not just premiums), so “insured” doesn’t still mean “one emergency away from debt.”

Fund reinsurance and other “shock absorbers” (state and federal) that reduce premiums by helping insurers cover very high-cost claims—similar to the kinds of state strategies described in recent reporting.

Lane 2: Pay less for the same care (the “price problem” fixes)

This is where the big health care savings live—because prices drive so much of total spending.

Stronger competition policy and anti-monopoly enforcement in hospital and physician markets, so dominant systems can’t just raise prices because they can.

Rate-setting approaches (various models exist): instead of every insurer negotiating separately, set or cap prices for certain services. The details matter, but the principle is simple: stop prices from being a black box that only big players can navigate.

Site-neutral payments (a technical phrase with a simple idea): if a service can safely be done in a lower-cost setting, don’t automatically pay more just because it’s billed as “hospital-owned.”

Lane 3: Make drugs cheaper (without killing innovation)

Negotiate more drug prices where public programs have leverage, and accelerate generic and biosimilar competition.

Crack down on pay-for-delay and other tactics that slow competition.

Improve pharmacy pricing transparency so patients and payers can see where markups and rebates are flowing (especially for high-cost specialty drugs).

Lane 4: Cut administrative waste and complexity

This is the unglamorous stuff that can still save real money.

Standardize billing and prior authorization rules across payers as much as possible.

Streamline enrollment and eligibility, so people don’t churn in and out of coverage due to paperwork.

Push toward simpler payment models where appropriate—because every billing rule has an admin cost.

A reminder: researchers estimate administrative health care spending is enormous in the U.S., on the order of $1 trillion per year. You don’t have to “solve” all of that to save big.

What about “Medicare for All” or a public option?

You can frame the big system choices like this:

Single-payer / Medicare for All (one main public payer):

Potential upside: simpler administration and stronger bargaining power on prices.

Potential downside: major transition, new taxes (to replace premiums), and political pushback.

Public option (a government-run plan offered alongside private plans):

Potential upside: can add competition and offer a benchmark price.

Potential downside: if provider prices stay high, the public plan inherits high costs too.

There’s no global consensus on the “one true model,” but the evidence is clear on one point: if prices and market power aren’t addressed, costs stay high—no matter who writes the checks.

What individuals can do (helpful, but not the main solution)

Systematic health care reform matters more than shopping tricks. Still, there are a few practical moves that can reduce your risk:

If you’re in a situation where you might face out-of-network billing (especially for emergencies), learn the basics of the No Surprises Act protections and dispute pathways.

Ask for in-network confirmation for planned procedures (hospital, anesthesiology, radiology—common “surprise bill” zones).

Use preventive care and chronic disease management aggressively. The boring stuff (blood pressure, diabetes control, screenings) is often the cheapest “cost reduction” there is—because it avoids catastrophic complications later.

The bottom line

If the enhanced ACA subsidies expire at the end of 2025, millions of people are likely to feel it quickly—through higher premiums, dropped coverage, or impossible household tradeoffs.

But the deeper fix to health care costs is bigger than subsidies: lower prices, reduce monopoly power, simplify administration, and pay for value instead of volume—while keeping coverage stable enough that people can actually use care before it becomes a crisis.

Moderate rain, with a high of 67 and low of 42 degrees. Fog in the morning, patchy rain nearby during the afternoon, overcast in the evening, patchy rain nearby overnight.